If you are a Realtor that sells condos, you know all about condo fees. The condo fees (aka maintenance fees, common expense contributions or strata fees) are the amount an owner pays, typically on a monthly basis, towards the cost of common expenses. And yet there is another significant element that requires your attention, as capital items are not paid for directly from the operating budget. Capital repairs and replacements are paid for out of a reserve fund that is built up from a portion of the condo fees. Any shortfalls are funded by special levies (aka special assessments).

So how is a Realtor supposed to know what these are going to be? Professional engineers estimate the useful life of each common element in a building and put together projections, often spanning 30 years. The engineer may also present multiple funding scenarios that illustrate how these capital items could be funded. These reports (called depreciation reports or reserve studies) are often hundreds of pages long, and are filled with material that is not easily understood by owners, buyers or Realtors.

Eli Report introduces its most powerful tool yet to simplify this: a special levy forecast. While our extraction is powered by AI, this feature is not a guess, it’s simple math using the best available information, displayed in a way that anyone can understand.

What exactly will Eli Report show?

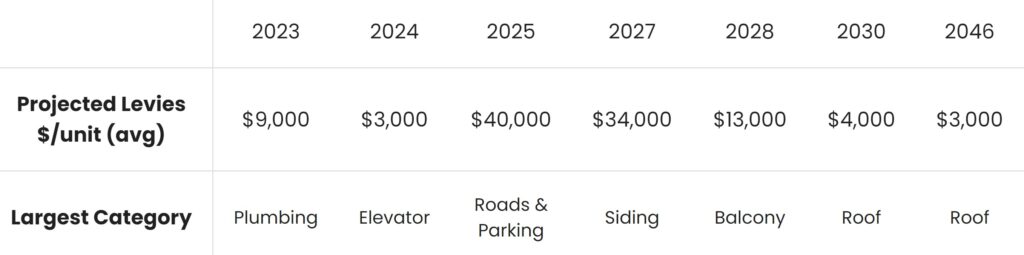

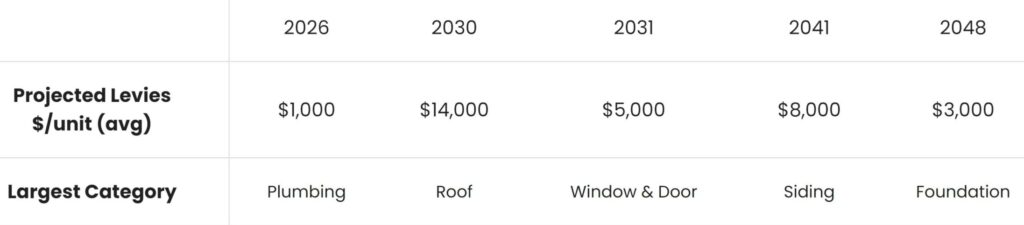

We are going to project the timing, amount and primary expenditure for special levies, shown on a dollar per unit basis (average). Depending on the nature of work being done, it may look like this:

This condo has some significant upcoming expenditures and not enough in its reserve fund. As anyone living in a multi-family community should know, having several special levies over the span of a few years does happen.

What does this mean to me?

As Realtor, this tool allows your clients to estimate the amount they may be asked to pay in a given year above-and-beyond the condo fees. While the special levy forecast is not perfect, it helps you convey the likely best-case scenario as far as financial exposure to maintaining the health of common property. In life, things tend to cost more and take longer than expected.

How will Eli Report justify this projection?

We do not provide any advice or opinions, so what is shown in the special levy forecast table will be derived from the data made available to us. These are the critical inputs:

1) Depreciation Report / Reserve Study

A depreciation report or reserve study is written by a professional engineer and should be updated at least every 3-5 years (various regions have different expectations, but the more often this is completed, the more reliable the estimated life and costs will be). We will use the projected expenditures estimated by the professional engineering company, which are adjusted for inflation on their assumptions.

2) CRF / Reserve Fund balance

We are provided with this figure on either financial statements or information certificate (known as a Form B in BC). If unavailable, our system will believe the CRF (contingency reserve fund) balance is $0 and overstate the amount of the first special levy accordingly.

3) Annual budget CRF contributions

While the depreciation report may provide several funding scenarios for the repair and replacement of capital items, it is our view that a reasonable predictor of future CRF contributions are the current annual budget CRF contributions. If this number is anomalously low or high in the latest budget available to us, the special levy forecast could be off materially.

Why might it go wrong?

There are many reasons our special levy forecast could be inaccurate, including but not limited to:

- being supplied with an outdated depreciation report, or only one depreciation report when there are more (sectioned stratas, amenity buildings, etc).

- capital replacement not happening on the schedule prepared by the engineering company in the latest available depreciation report

- inflation meaning that costs are higher (or lower) than estimated by the engineering company in the latest available depreciation report

- a strata choosing to increase (or decrease) the rate of CRF contributions

- the latest budget CRF contributions not being reflective of a typical budget year

- the latest CRF balance excluding funds set aside for capital projects (we can display the forecast with total reserve funds)

- a strata earning more or less on their CRF balances (we do not initially assume any rate of interest earned on CRF funds, though may support that in the future)

- a larger or smaller special levy being raised by the strata, meaning that they have more or less funds at a given point in the future

- bad data from extraction, or human error from a failure to accurately review that data

- sectioned stratas having more than one depreciation report or budget, which may cause us to present a partial picture

- a natural disaster, catastrophe, act of terrorism or otherwise that accelerates near-term capital expenditures

- inaccurate building information (such as the number of units) may cause us to under or over-state the levies on a per unit basis

- the average presented is based on the number of units, not a specific unit or entitlement, so if you own a penthouse your levies will be relatively higher, and if you own a studio your levies will be relatively lower.

As a result, while this tool is designed to give you and your clients at least a good sense of exposure to special levies, it is important that Realtors always read the underlying documents and provide their clients with suitable advice. Eli Report assumes no liability for any inaccuracies in the collection, presentation or display of data.

If you are a Realtor, owner or buyer into a multi-family community, sign up and get a free Eli Report (special levy forecast optional).